Managing money can be challenging, especially for beginners. Many people fall into the same traps that keep them from reaching financial stability. The good news is that once you identify these mistakes, you can take steps to avoid them and build a healthier financial future.

Here are ten of the most common money mistakes and how to fix them.

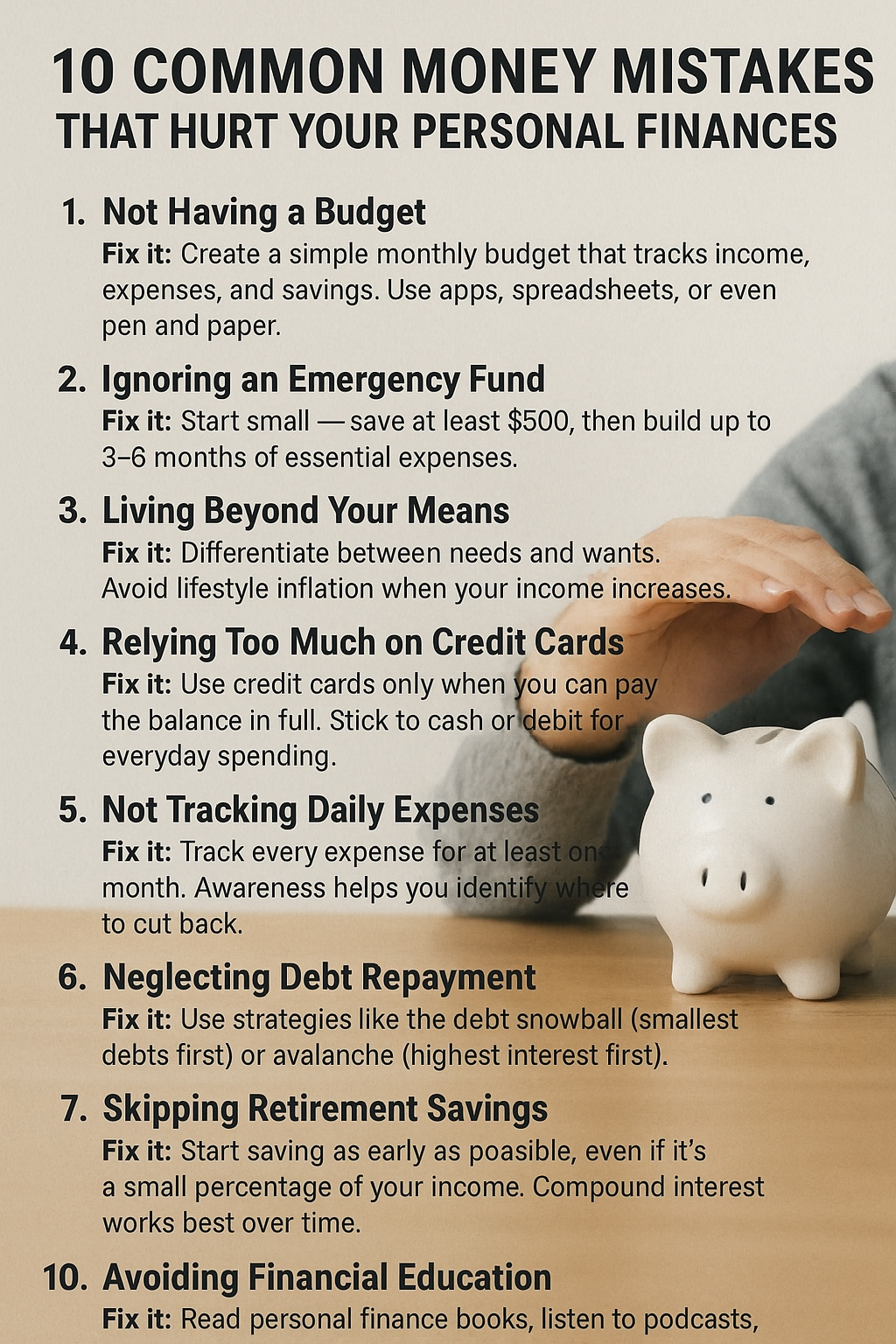

1. Not Having a Budget

One of the biggest mistakes is living without a plan. Without a budget, it’s easy to overspend and wonder where your money went.

Fix it: Create a simple monthly budget that tracks income, expenses, and savings. Use apps, spreadsheets, or even pen and paper.

2. Ignoring an Emergency Fund

Life is unpredictable. Without savings for emergencies, people often rely on credit cards or loans when unexpected expenses arise.

Fix it: Start small — save at least $500, then build up to 3–6 months of essential expenses.

3. Living Beyond Your Means

Spending more than you earn is a fast track to debt. Even small overspending habits add up over time.

Fix it: Differentiate between needs and wants. Avoid lifestyle inflation when your income increases.

4. Relying Too Much on Credit Cards

Credit cards can be useful, but using them to cover daily expenses without paying the balance can trap you in high-interest debt.

Fix it: Use credit cards only when you can pay the balance in full. Stick to cash or debit for everyday spending.

5. Not Tracking Daily Expenses

Many people underestimate how much small purchases — like coffee or snacks — impact their budget.

Fix it: Track every expense for at least one month. Awareness helps you identify where to cut back.

6. Neglecting Debt Repayment

Carrying balances on loans or credit cards without a repayment plan can drain your finances through interest.

Fix it: Use strategies like the debt snowball (smallest debts first) or avalanche (highest interest first).

7. Skipping Retirement Savings

Many people delay retirement contributions, thinking they’ll start later. The problem is that time is your biggest asset.

Fix it: Start saving as early as possible, even if it’s a small percentage of your income. Compound interest works best over time.

8. Impulse Buying

Buying without planning can blow your budget. Retailers use marketing tactics to encourage impulse purchases.

Fix it: Wait 24 hours before making non-essential purchases. This reduces emotional spending.

9. Not Having Clear Financial Goals

Without goals, it’s easy to lose focus and spend money without purpose.

Fix it: Set short-term, medium-term, and long-term financial goals. This gives your money direction and meaning.

10. Avoiding Financial Education

Many people avoid learning about money, thinking it’s too complicated. But ignorance often leads to costly mistakes.

Fix it: Read personal finance books, listen to podcasts, and follow reliable financial educators online.

Final Thoughts: Small Changes, Big Impact

Everyone makes money mistakes, but the key is learning from them. By avoiding overspending, building an emergency fund, repaying debt, and setting goals, you can take control of your finances.

The sooner you identify these habits, the sooner you can replace them with smarter financial choices — and the more secure and stress-free your financial future will be.